Axon Enterprise - To Protect and Serve

Company Introduction:

Axon Enterprise, Inc. (NASDAQ: AXON), headquartered in Scottsdale, Arizona, is a leading technology company specializing in law enforcement and public safety solutions. The company was founded in 1993 by Rick Smith and his brother Tom as TASER International, with the mission of developing non-lethal alternatives to firearms to reduce gun-related deaths in police encounters.

While the company initially faced legal challenges due to injuries associated with its TASER devices, it gradually gained widespread adoption as law enforcement agencies recognized the value of non-lethal force options. Over time, Axon expanded beyond its core TASER product, introducing body-worn cameras and in-car fleet systems to enhance transparency and accountability in policing.

Recognizing the growing need for data management and analysis, Axon launched Axon Evidence, a cloud-based platform that helps law enforcement agencies store, organize, and analyze massive amounts of digital evidence. This system streamlines police reporting, accelerates case processing, and integrates artificial intelligence tools to extract insights from recorded data—marking one of the first real-world applications of AI in law enforcement. Today, Axon continues to innovate at the intersection of hardware, software, and AI, shaping the future of public safety technology.

Products & Services:

Hardware: Manufactures Tasers, body-worn cameras, Axon Fleet in-car systems, drones and Anti-drone equipment.

Software & Services: Provides digital evidence management solutions (e.g., Axon Evidence), cloud-based analytics platforms, and VR training services.

Geographics:

Operates primarily in the United States with an expanding international footprint to serve global law enforcement agencies. In 2023, international accounted for 14% of its sales.

Competitive Advantages:

I believe Axon is a SaaS business with a hardware moat, entrenched in the mission critical public safety sector, that have a 125% Revenue Retention Rate and $14.5bn backlog . It is One of the best cases of commercially successful application of AI reshaping law enforcement agencies, delivering measurable ROI to clients.

Integrated Ecosystem of Hardware, Software, and Cloud Services creates high switching cost: Axon offers a comprehensive suite of products, including TASER devices, body-worn cameras, and the cloud-based digital evidence management platform, Axon Evidence. This seamless integration enhances operational efficiency for law enforcement agencies and makes it really hard to switch to another provider.

Strategic Upselling to Existing Customers: By continuously introducing new services and solutions, Axon effectively upsells to its established customer base, fostering long-term relationships and generating recurring revenue streams demonstrated through best in class 125% NRR.

Strong Customer Relationships and Brand Recognition: With a mission to "protect life, capture truth, and accelerate justice," Axon has built robust relationships with law enforcement agencies and government institutions over decades, becoming a trusted partner in public safety. The regulatory barrier prevents AI native competitors from entering easily.

Major Customers:

Predominantly law enforcement agencies both state and federal level, and adjacent public safety organizations like corrections facilities in the U.S. and internationally. Also trying to expand to corporate clients like retail and logistics.Major Suppliers:

Primarily manufactures in the US at the Scottsdale facility. Software center based in Seattle.Senior Management & Board of Directors:

Senior Management: Led by CEO Rick Smith, supported by a team of experienced executives in technology, operations, and finance.

Board of Directors: Comprises seasoned professionals from technology, law enforcement, and financial backgrounds who guide the company’s strategic direction.

Strategic Acquisitions:

Dedrone (May 2024): Axon announced a definitive agreement to acquire Dedrone, a leading counter-drone technology company. This acquisition aims to enhance Axon's ability to detect and mitigate unauthorized drones, integrating Dedrone's solutions into Axon's public safety platform.

Fūsus (2024): Axon acquired Fūsus, a company specializing in real-time crime centers for public safety agencies. This acquisition expanded Axon's market opportunity by over $3 billion in both U.S. state and local government sectors, as well as international markets.

Line Item Discussions:

Revenue - The Hardware Segment

Axon’s revenue can be split to three categories: Tasers (Tasers, cartridges, training services) Sensors (Fleet camera, body camera, other accessories) and Axon Cloud (Evidence.com, Draft one AI assistant).

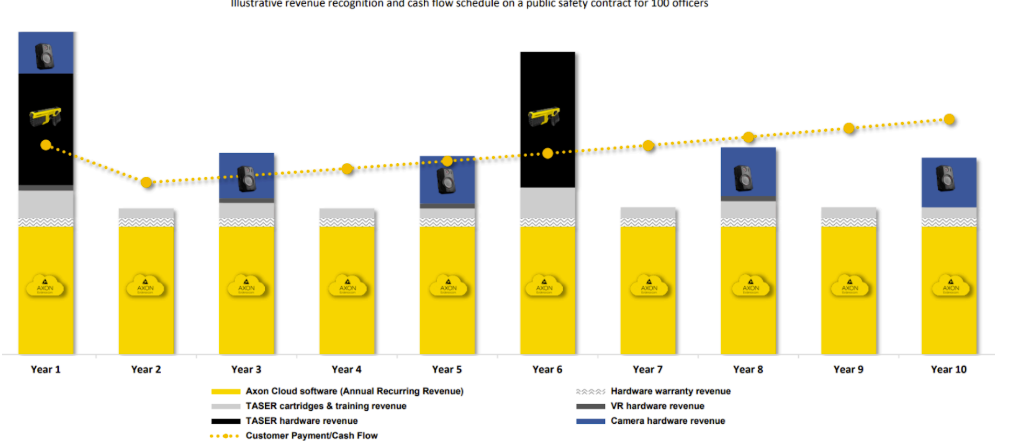

Tasers and Sensors are the hardware segment. As new products are launched, depending on their usefulness, they will get different adoption rates. For example, Axon had a really strong adoption of Taser 10 due to its longer range and higher voltage. The product cycle has a lot more visibility since customers are subscribed to the Axon program, which upgrades Taser every five years and Body camera every two years. As of May 2023, Axon Enterprise reported that 63% of its TASER devices were sold through subscription plans.

Axon is encouraging its customers to transition to a subscription model because it gives customers access to the latest technology without having to go to city counsel and ask for budgetary approval for every new purchase. The subscription model integrates both hardware and software as an operating cost embedded in the annual budget, so there are no surprises to the budget counsel and it gives the police department access to the latest technology to protect their employee on the field. This model also gives Axon and investors more visibility into future revenue numbers as they are reported in the booking in multiple year contracts.

When we examine the growth drivers of the hardware segment, it’s mostly coming from renewing product cycles and signing up more agencies to its subscription plan to encourage higher product turnover. There remains plenty of room for innovation for advanced Tasers weapons since the current Taser gun has a 80% effective rate due to heavy clothing and cartridge malfunction. It cannot be used as the primary weapon of choice, it's mostly used when the other officer is covering a Taser shooter with a rifle. Axon’s goal is to make lethal weapons obsolete in law enforcement and self defense, there remains a long road ahead to achieve this goal.

The Overseas market remains an opportunity, but due to regulatory barriers and higher competitive pressure its growth remains lackluster and volatile (sold in bulk) compared to domestic sales growth, so in my model I assume foreign sales grows at historic growth rates and its percentage of revenue will decline overtime as domestic sales grows faster.

Axon recently added new features such as AI two way translation, live streaming and automatic recording to its cameras, highlighting the software side is way more important than the hardware itself, and Axon is the best at custom building technology for law enforcement. I view the adoption of body cameras quite favorably because it creates more data that needs to be stored and processed on the cloud. When Axon controls the hardware, it controls the software to create a seamless experience for its customers and a barrier of entry to pure play cameras or software providers.

There are also new products like Drones and De-Drone that are being actively developed and adopted by clients. In future we believe humanoid robots could serve as patrolling officers too. Technology is evolving rapidly and Axon is bringing key innovations to law enforcement agencies. The product pipeline remains robust.

Projections:

For the Tasers segment, the business remains relatively stable. It was revitalized recently by the introduction of Taser 10, it’s only 2 years in the 5 year product cycle so I believe the growth momentum is still strong and more customers will adapt to the new product either through subscription plan or bulk purchasing. Civilian defense and oversea contracts remain promising, axon has been talking about unveiling a taser that is as good as a gun in the next couple of years, although it’s still in the developmental phase the results have been promising. If that can be successful I expect Tasers to tap into a much larger TAM and produce significant growth. So for the upside I chose 20% annualized growth, base case where the new Taser were not released would be 15% and down case the new product was a failure and Axon was unable to release more innovative products, I assign a growth rate of 15% reflecting price increases and incremental improvements.

For the Sensors Segment (Body Camera, Fleet Cameras, etc.) I underwrote 20% annual growth for base case, continuing last year's growth trend reflecting a long tail of smaller law enforcement departments adopting body cameras and fleet systems. For the upside case I consider the adoption of body cameras in retail and healthcare where workers are subject to frequent assault. There could be further adoption coming from international police departments as citizens demand for transparency in law enforcement grows stronger, so I am assigning a 25% growth rate. And I assigned 15% for a downside scenario potentially caused by competition from motorola and uncertainty around the breakup with Flock which specializes in license plate identification and safety cameras. This could cannibalize Axon’s fleet system.

The Cloud business:

Axon offers a variety of Cloud services from Evidence.com as the largest law enforcement data storage website to software like Draft One that uses LLMs to help officers draft up reports and Redaction and evidence management tools that automatically processes the evidence for officers. When projecting Axon’s cloud business, I use the following equation:

Total Cloud Revenue = (Number of Subscribed Agencies) × (ARPU) × (Renewal Rate + Upsell Growth

Subscriber Base Expansion:

The company does not publicly break out the exact percentage of those hardware subscribers who have not also subscribed to its cloud services. However, industry analysts estimate that roughly 20–30% of agencies that purchase Axon’s hardware on a subscription basis have not yet adopted the company’s full suite of cloud-based offerings (such as Axon Evidence and Draft One AI assistant). This represents a significant upsell opportunity for Axon to convert more hardware customers into integrated users of its cloud ecosystem.

Police departments are finding it difficult to retain its officers as it's a dangerous job that deals with constant stress. The headcount for the police department did not expand yet the budget on public safety increases in-line with inflation and is not expected to be cut. So more of this budget will be directed towards technology as a force multiplier to enhance officers’ capacity to process more cases efficiently, which benefits the largest service provider - Axon.

Average Revenue Per User (ARPU):

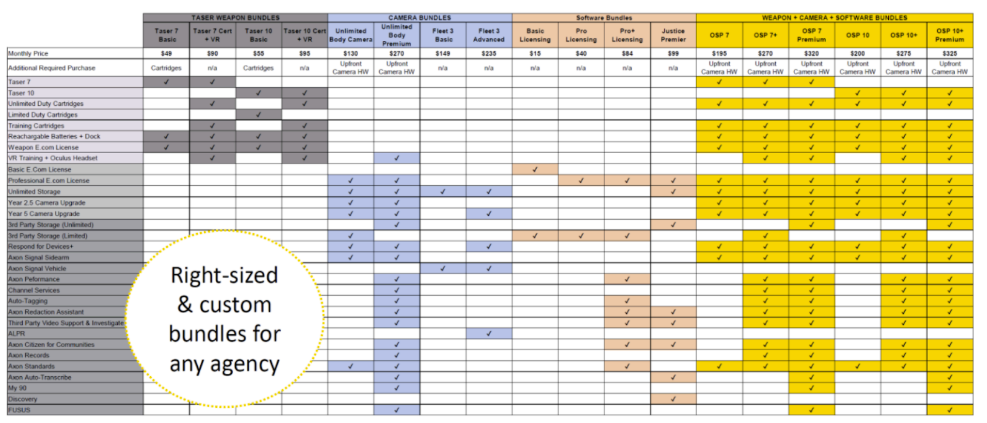

Axon uses a price per headcount model and The OSP 10+ Premium bundle is now $325/month and includes every product. This tier has increased over time, up from $299 in 2023, $249 in 2022, and $199 in 2019.

Axon has many opportunities to raise the subscription price by upselling existing customer base with newer features. Having AI write the reports and having the tools necessary to process the video images collected are a huge time saver. The saved time alone would justify upgrading to a premium tier because the policemen's overtime pay is around $50 an hour. The software subscription costs $50 a month, so just by saving one hour per month the department was able to make back the cost. Customers have embraced software innovation. The results have been impressive with ~50% time savings, which is force multiplier and directly translates into more officers on the streets

Renewal and Churn Rates:

Government contracts are very sticky with high renewal rates (with estimated churn below 5%), which enhances revenue visibility over multi-year contracts. Axon has an NPS score above 80.

Revenue Retention rate is 125% which means every five years (one product cycle) customers opt to double the subscription size, based on the service axon delivered.

Projections:

I believe axon will continue to add new service options that address customer pain points thus raising the price ceiling of its subscription plan while getting more customers to adapt its software plans. Customers only chose the services that they wanted, delivering customer value while convincing customers to further migrate more of its software stack to Axon’s host of solutions.

The Cloud business, for the upside case I am projecting it to grow at 35% annually driven by higher adoption and upselling new features. For base case I am assuming a 30% growth rate in cloud, and for bear case I assume the growth will decelerate as Axon failed to introduce more innovative solutions to address client pain points, so from 30% in next two years to 25% in future.

Cost of Goods Sold:

Axonreports Taser segment and Cloud+Sensors segment, combined their gross margin are similar around low 60s range. However, if we further break up the segments to view cloud service as a standalone segment, its margin is the mid 70s. Sensors like body cameras, due to their competition, have lower margins at around the low 40s range.

Tasers have been very successful, maintaining gross margins in the 60%s range demonstrating Axon’s first comer advantage and leading product innovation. I believe the margin profile for Axon’s different segments are unlikely to change as the defense industry enjoys a high barrier of entry and low incentive to haggle on price since its government contracts. If cloud providers like Amazon increased their hosting fees, Axon can pass that to the client. So for the upside I put 66% gross margin for the software and sensors segment, reflecting an increasing cloud margin in the mix. And for Taser I put 66% if Axon was able to raise its margin by raising price. For base case and down case I kept them at the same levels, 62% and 60%.

I think overall Gross Margin will gradually expand as cloud services ramps the fastest and takes a bigger share of revenue. Cloud service is more profitable so it will lift the gross margin. And investors are pricing in this shift in revenue profile and assigning Axon a Saas comparable set and multiple.

Long Term Ebitda guidance:

Management has guided long term EBITDA margin to be 28% in their recent report (Raising prices, fixed cost leverage from its manufacturing facility). I believe it’s doable and this is what I assigned as terminal ebitda margin for the company. I expect a gradual ladder up from 25% to 30% in the next three years.

Research and Development there might be incremental cost savings but it will largely remain high since the company is transitioning to a technology service company. For the upside I expect a gradual decrease as a percentage of revenue from 14.7% to 14%. And for the base case I expect R&D to remain the same 15% all years. And for downside I put 17%, which might not mean a bad thing because I consider research and development expense an investment into the long term, even though many results were intangible and expensive, I still think it’s because companies want to invest in the future growth.

On the SG&A side, I don’t think it will change dramatically as well. Other cloud providers all report high 20%s SG&A. Axon has sales representatives visiting police departments to check-in and upsell their new services, they also have a legal team for potential lawsuits, and they have a share compensation plan that every employee can choose to subscribe to, as the share price appreciates, the share based compensation expense increases. So overall for the upside I forecast it to gradually decline from 28% to 26%, for base case I wrote 27%, and for bear case I said remain the same, reflecting no leverage effect due to cost overruns.

Earnings Power Discussion: How big is the market and how well can axon capture it?

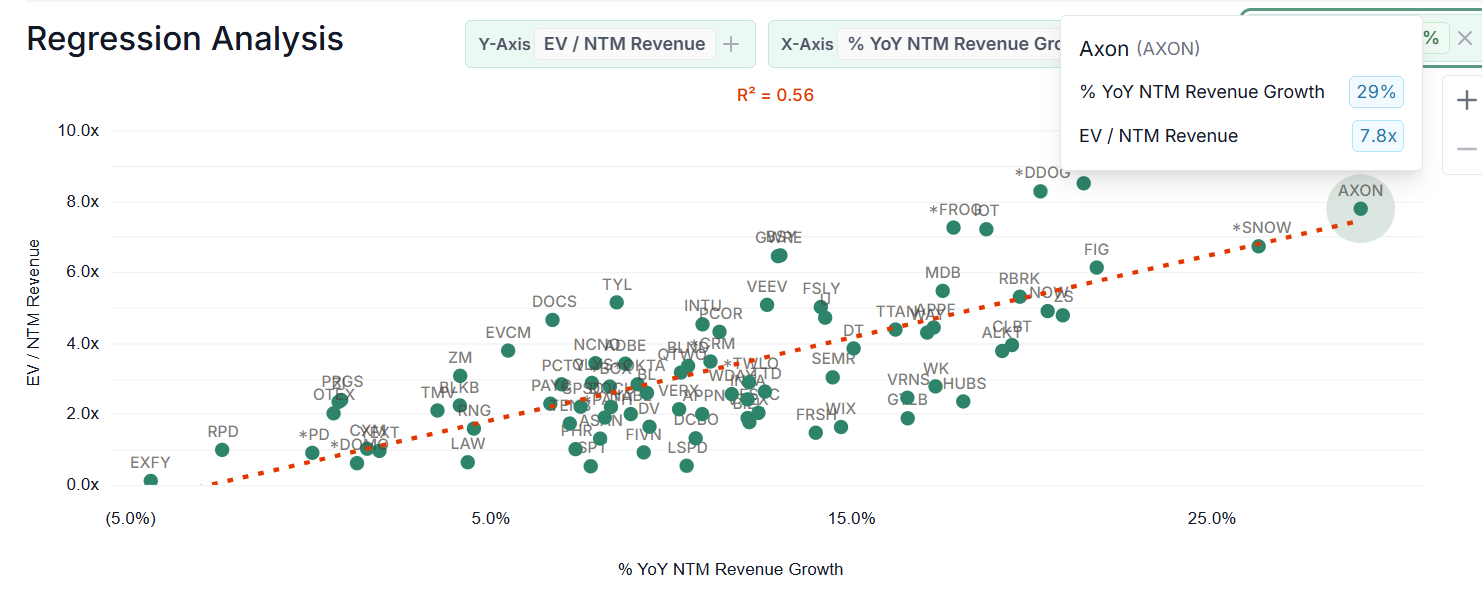

Axon is one of the best names that demonstrated success in applying AI in the law enforcement space. Before the pullback, its lofty valuation requires further justification. Now the valuation is a lot more attractive, EV/NTM Sales ratio around 8x and Price to adj.earnings around 50x, scoring right on the regression line when compared to comp SaaS peers.

And to project five years ahead we need to examine how big is the addressable market and how likely will Axon continue to expand on these verticals.

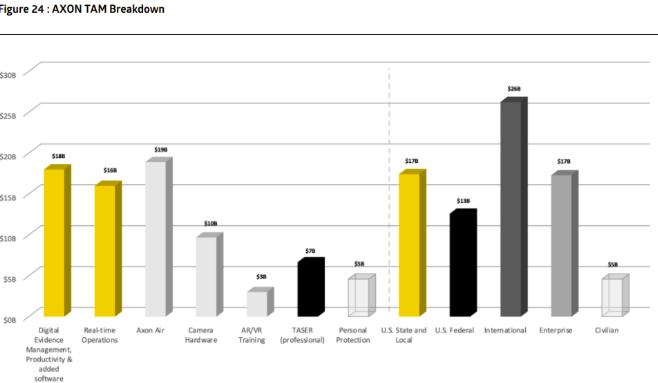

The immediate addressable market would be the U.S. State & Local at $17b, including 900k+ law enforcement personnel between sworn and civilian roles, and 400k+ vehicles. And there are expansion opportunities such as international sales, and enterprise level most notably in industries subject to crimes like retail and healthcare.

And when we look at the expanding product verticals, Axon has been making acquisitions to expand its TAM. For example the acquisition of Fusus real time crime center added $16B in TAM, and developments in the drone and dedrone vertical added $19B in TAM. The most important vertical is the digital evidence management and productivity added software, its TAM can grow infinitely larger as Axon develops more software that addresses customer pain points and delivers value.

Axon’s products deliver tremendous customer value and have a NPS score above 80 and a 122% Revenue Retention Rate, which means every five years when a customer renews his contract its value increases by 2x. Customer checks conducted by research agencies have been very positive and users are praising Axon for bringing forefront technology to this highly sensitive and inefficient industry, making the law enforcement more transparent and speeding up the justice process through its data collecting and analyzing tools.

Axon has a $20B+ TAM and its current revenue is $2B. It has only penetrated 10% of its TAM and has a long runway to further grow its earnings. The defense industry has a high barrier of entry and Axon’s subscription business model further enhanced customer stickiness. The most important part comes from Evidence.com and data analysis tools like AI enabled Draft One that comes with the platform. It’s incredibly costly and the switching cost can be prohibitive for customers to migrate to another platform to store its data on cloud and offer the software that its staff are used to using. As a SaaS business Axon enjoys decreasing marginal cost.

And the law enforcement space has a highly stable budget that is unlikely to be affected by DOGE cuts, this gives investors more certainty that the customer demand will always be there and they are great customers that never default on bills.

Additional Growth Options: Autonomous Humanoid policing robots

Given Axon’s unique advantage—boasting the largest law enforcement databases for training advanced AI models—there is significant potential to leverage these assets. I am particularly curious if Axon intends to integrate technologies similar to those developed by Tesla in autonomous driving and humanoid robotics. Such an initiative could result in a policing robot capable of robust, real-time decision-making and enhanced operational efficiency. If this thesis is proven, axon could be one of the largest defense contractors for supplying robot enforcement officers and soldiers to the army.

I don’t think the market currently assigns any valuation towards this possibility and this could be the biggest catalyst to the company if it were proven in future. I did not assign any value to this as it is not yet material.

Valuations

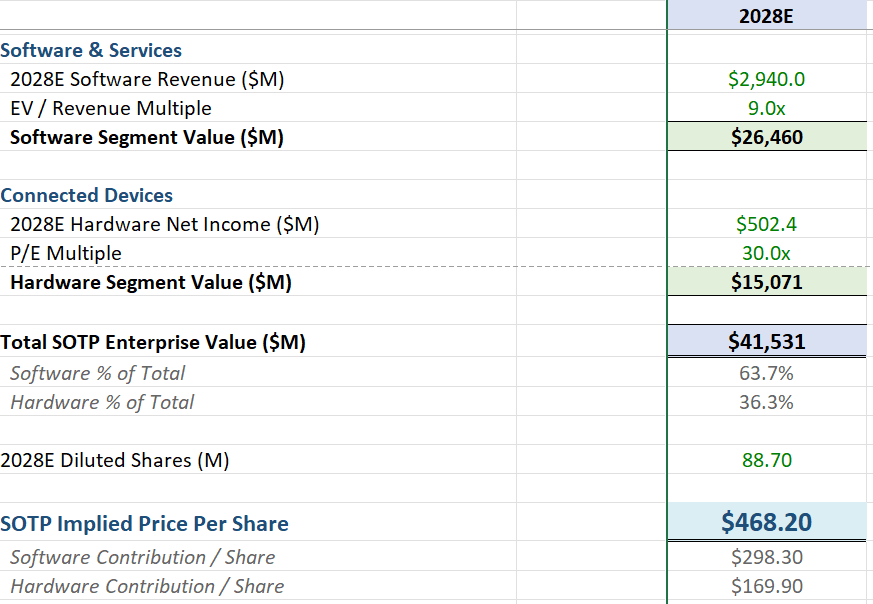

We decided to do a sum of the parts valuation for Hardware and Software segments since that more accurately reflects their growth prospects and business lines. For hardware the closest comp is Motorola Solutions public safety segment valuation, I put a 30x pe. For software I believe it’s mostly in-line with the SaaS peers, assuming no material de-valuation from this point, which is a big uncertainty given how irrational market reacts when it comes to this sector.

We are seeing a ~30% upside potential from this price point, we view Axon favorably as the business will not be disrupted by AI, it’s a key beneficiary from it. However due to sector volatility, the traditional Price to Sales valuation is being questioned and investors are resorting back to PE or ev/adj.ebitda to value SaaS businesses. We would like to see some stabilization before entering a position.