Tsugami China: A High-End Machinery Provider Enabling Robotics, EV & AI

Tsugami China (01651) is a Hong Kong–listed name I discovered through a stock screener. After digging into the fundamentals, I believe the valuation is reasonable, the industry has high barriers and attractive long-term demand, and the company stands to benefit from growth in AI liquid cooling, robotics, and new-energy vehicles—segments that all require more precise and more capable machining equipment. Recent geopolitical tension between China and Japan has dragged down the share price, creating an appealing entry opportunity. If Tsugami is eventually included in the Stock Connect program, it may see a valuation re-rating.

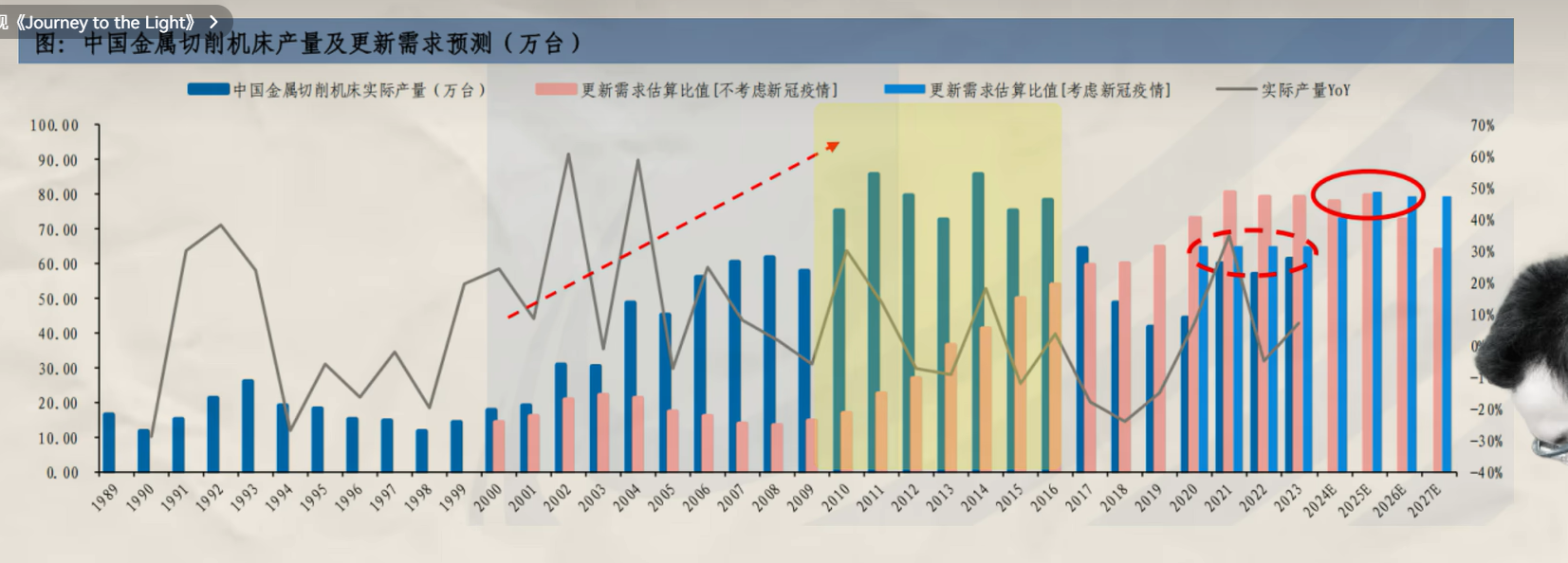

As the so-called "mother machines" of industrial production, machine tools form the basis of all manufacturing and move closely with the macro cycle. Meanwhile, the rapid growth of NEVs, AI hardware, and robotics has structurally lifted demand for high-precision, high-efficiency equipment. Therefore, the sector combines cyclical fluctuations with clear structural growth. China's machine tool industry bottomed out in 2019-2020, moved into an upcycle in 2020-2022 on the back of industrial upgrading, strong exports, and accelerating import substitution, and then softened in 2023-2024 as macro demand weakened and manufacturing investment confidence fell due to trade wars. Entering 2025, the market has become significantly bifurcated: the low end is intensely competitive and mired in a "revenue without profits" dilemma, while high-end machine tools-underpinned by NEVs, AI servers, aerospace, and robotics-are the first to recover. Their growth is shifting towards a higher gear as these are highly profitable industries with huge potential demand.

Tsugami China is the core Chinese subsidiary of Japan's Tsugami Group and is different from ordinary foreign brands operating in China. It combines a powerful Japanese brand heritage with deep local production and service capabilities, creating a business model that competitors cannot easily imitate. The company carries forward Tsugami's 86 years of technical expertise, owns all rights to the TSUGAMI brand rather than importing products, has invested heavily in local manufacturing in Pinghu, Zhejiang, and created a comprehensive service and customization network responding far faster than foreign brands that rely on distributors.

In the Chinese market, Japanese and Korean brands have gradually replaced Western brands as the top tier, while Chinese machine tool makers are moving from low/mid-end up toward the high-end segment and growing exports. Machine tools are a core indicator of a country's industrial strength, and with Western industrial capacity shrinking, global demand is increasingly shifting toward China, Japan, and Korea. As the world's largest manufacturing base, China naturally has the strongest demand for machine tools.

On domestic substitution risk, Tsugami confronts a structurally favorable competitive landscape. Tsugami is the clear segment leader in China's high-precision small-lathe market, with roughly 60% share. This advantage comes from its deep process know-how in precision automatic lathes, particularly in small-part mass production where precision retention, stability, and efficiency matter most; highly localized operations that compress costs and enhance responsiveness; and a sticky customer base across automotive, medical, IT, and other high-spec manufacturing, where switching costs are high. In addition, on China-Japan geopolitical risk, the two economies remain deeply complementary in manufacturing. Tsugami China is a long-established, fully onshore operating entity, and the practical impact on day-to-day business is likely limited.

The sector today is in the early stage of a bottoming recovery, with clear divergence. Manufacturing PMI stayed below the expansion threshold for months in 2025, signaling soft overall demand. Competition is fierce, pressuring margins across much of the industry. Even leaders like Haitian Precision posted "revenue up, profit down," with revenue up 1.13% but net profit down 16.39% in the first three quarters of 2025. Underneath this, the K-shaped divergence is clear: the low-end segment suffers from price wars and margin compression, while high-end applications tied to NEVs, AI, aerospace, and robotics show early signs of recovery. This divergence is echoed in the product mix at industry peer DMP: its 3C product line, down 42.21% in 2023, rebounded 153.29% in 2024, while general-purpose products continued to decline. Downstream demand is shifting toward emerging manufacturing, and recovery in high-spec equipment is materially stronger.

Machine tools have an 8-10 year replacement cycle. The previous peak was in 2011-2012, so 2021-2025 should have been a new upgrade cycle, but it was delayed by macro uncertainty. With policy support for equipment renewal and structural demand from high-end manufacturing, the new cycle is gradually starting but is likely to be an "L-shaped slow lift" rather than a sharp V-shaped rebound.

The core product of Tsugami is precision lathes, especially precision automatic lathes used for high-volume, high-precision production of small rotational parts. These machines are irreplaceable in auto components, medical devices, precision transmission, and other fields. More than 86% of Tsugami's revenue comes from precision lathes, with automotive being the largest downstream at approximately 44%. The dependence on the more volatile 3C electronics sector is only 7–8%, enabling the company to avoid the cyclicality of that segment while benefiting from the electrification and intelligentization of EVs.

Tsugami has also positioned itself well in emerging fields. With AI computing demand surging, liquid-cooling hardware is becoming critical; precision pump shafts and valve components in cooling systems are ideal applications for Tsugami’s lathes and represent a significant growth driver. In robotics, joint modules and core transmission components require extremely high machining accuracy, aligning perfectly with Tsugami’s strengths. In high-end medical equipment, surgical robots and advanced devices use precision metal parts that also require high-accuracy turning. Analysts estimate that at a production scale of one million humanoid robots, the demand for equipment to produce planetary roller screws and harmonic reducers alone could exceed RMB 23.5 billion; by 2030, related lathe and grinder demand could surpass RMB 5 billion annually, with total component-related machine tool demand easily exceeding RMB 10 billion. This hardware intensity will force a “precision revolution” in machine tools and structurally lift demand for high-end equipment.

Companies like DMP, however, focus more on machining centers for 3C structural parts and generic housings and casings, complementing Tsugami instead of competing directly against it.

Financially, Tsugami shows clear premium economics. Gross margins are maintained well in excess of 30% (32.1% for 1H FY2025), materially ahead of comparators such as DMP at around 25% and Haitian Precision at around 26%. Its net margin reached 17.2% for the same period, versus Haitian at 13.42% (and falling) and DMP at below 10%. During the downturn in 2023–2024, Tsugami even managed to improve its gross margin through stringent cost management, which reflects strong operational resilience. All this is indicative of its segment dominance, technical barriers, and brand premium. Tsugami remains insulated from low-end price wars and is continuing to showcase excellent cost control and operational efficiency. Gross margin, net margin, and inventory turnover all continued improving, pointing to strong business momentum.

Capacity expansion—its new plant in Pinghu will lift production—will continue to underpin future growth, alongside deeper penetration in emerging sectors such as NEVs, AI liquid cooling, and robotics, plus ongoing import substitution. Even at the high end, Tsugami retains a cost-performance and localization advantage over Japanese and Swiss competitors. The addressable market remains large.

Catalysts

Tsugami is not currently part of the Hong Kong Stock Connect program, which has kept its valuation conservative. While peer A-share machine tool companies tend to trade at richer multiples, Tsugami's multiple stands at about 10-12x earnings, compared to the A-share peer average. Given the leadership position and strong profitability, and considering exposure to fast-growing sectors, there is room for normalization. I think the stock could reasonably re-rate to 15x or above, though its inclusion may depend on reaching the HKD 8 billion market-cap threshold. On a December average, it may not meet the March review, but it could satisfy the criteria by the September review. Trading liquidity is healthy, and the share price has been active since the earnings recovery began. With the sector now entering a new mild upcycle, and Tsugami continuing to expand its footprint in high-end manufacturing, the company should be a beneficiary of both the cyclical recovery and structural growth, giving room for earnings and valuation upside. The core investment merits for Tsugami include its c. 60% share of China's precision automatic lathe segment, very strong profitability with gross margins above 30% and net margins above 17%, healthy downstream exposure to autos and new-economy manufacturing, deep positioning in AI liquid cooling and robotics, and a valuation that appears undemanding, with potential for re-rating once Stock Connect inclusion is attained.

Key risks include weaker-than-expected macro recovery, rising industry competition, delays in Stock Connect inclusion that could prolong a liquidity discount, and geopolitical uncertainty. Overall, Tsugami China stands out as the leader in its high-precision niche. Technical strengths, brand premiums, and strong profitability give it high resilience, while the secular rise of AI hardware, robotics, and NEV manufacturing should continue to amplify demand for precision machining.

Earnings stability and long-term growth seem well supported. According to the company's results, Tsugami plans to distribute a final FY2025 dividend of HKD 0.50 per share, higher than last year's HKD 0.40 and above the interim HKD 0.45. The full-year dividend of HKD 0.95 is a record high, roughly a 3% yield. In addition, management has repurchased 2.371 million shares in April and May, signaling management confidence and helping stabilize valuation while lifting EPS and book value per share.