Duolingo: Mispriced AI Beneficiary

Duolingo’s 70% correction from its peak has created one of the more compelling dislocations in AI enabled software. At first glance, the selloff appears tied to a conventional “growth to value” transition: lowered guidance, softer DAUs in its most mature markets, and widespread fears that rapidly advancing AI models may erode Duolingo’s competitive advantage. Yet a closer examination shows that the market has misread a strategic rebalancing as structural decline, and that Duolingo’s core economics, product defensibility, and AI-enabled optionality remain not only intact but accelerating.

To understand why this moment represents a genuine mispricing, it helps to examine what originally made Duolingo a premium-valued compounder. The company operates in one of the largest consumer TAMs on earth—over two billion people learning a second language—with demonstrated cross-cultural product-market fit. Nearly 60% of revenue today comes from outside the United States, and China, already about 5% of revenue, has become one of the company’s fastest-growing markets. This global breadth is not accidental. Duolingo designed a product that travels extremely well: short-session, gamified, mobile-first, and built around universal psychological motivators rather than curriculum styles dependent on any one national education system.

Economically, Duolingo resembles a software and mobile gaming hybrid—high-margin, highly scalable, and powered by organic user acquisition. Gross margins hover above 70%, adjusted EBITDA margins approach 30%, and nearly 90% of user acquisition is organic, driven by social virality and behavioral reinforcement. Once courses are created, the marginal cost of serving an additional learner is effectively zero. In other words, Duolingo was always valued less like an education company and more like a subscription consumer platform with unusually durable engagement mechanics.

Crucially, Duolingo solved the behavioral bottleneck in adult learning. Traditional EdTech failed because it assumed motivation; Duolingo built motivation directly into the product. Streaks, XP, leaderboards, and micro-lessons transformed language study from discipline-based effort into a repeatable game loop. The result has been consistently rising DAUs, expanding cohort retention, and steadily improving conversion into paid subscription tiers. These fundamentals—user habit formation and unit economics—have not changed.

The Drawdown

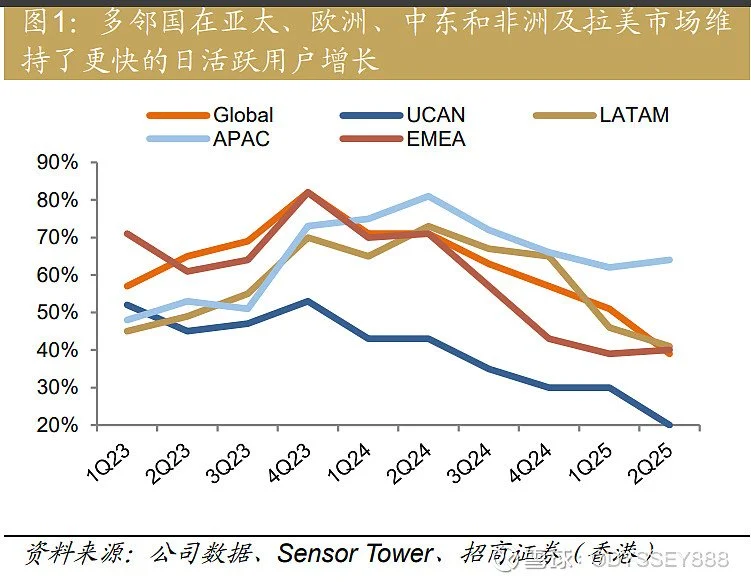

So what explains the 70% drawdown? Not AI disruption. Not competitive erosion. Instead, management chose to prioritize long-term DAU growth and pedagogical improvement over near-term monetization. This created short-term pressure—particularly in UCAN, Duolingo’s most mature region—and led to lowered guidance. But the strategic intent could not be clearer. Management has repeatedly emphasized the goal of maximizing long-term lifetime value, even at the cost of near-term revenue softness: “We are investing in the long term,” “We want to grow DAUs fast for a very long time,” and “If we teach better, user growth follows—but with a lag.” Investors, conditioned for short-term subscription acceleration, reacted poorly. But the behavior itself is consistent with other platform companies that suppressed very short-term financial results in order to optimize for much higher, more durable monetization later.

Historical analogues illustrate this dynamic. FICO spent years underpricing the most essential consumer scoring product in the United States. Once it activated pricing power, the stock compounded over 20x. Netflix was pronounced “finished” every time user growth decelerated, yet each S-curve transition—from DVDs to streaming, domestic to international, content licensing to originals—unlocked new long-term value. Duolingo’s strategic shift today rhymes with both cases: a platform strengthening its core before deploying monetization levers that grow significantly more powerful at scale.

On AI

The market’s second major concern—AI—has also been misunderstood. Large language models can converse, but they cannot teach. They lack sustained curricula, scaffolding, ability to diagnose skill levels, calibrate difficulty, or sustain motivation. Duolingo’s moat does not depend on model ownership; it depends on proprietary learning-state data and a pedagogical workflow no foundational model can replicate. Millions of learning trajectories—mistake patterns, retention triggers, fatigue curves, speech samples—feed into a system that personalizes lessons and optimizes reinforcement. This dataset is not just large; it is deeply structured around the act of learning, rather than the act of predicting text. As with Axon, whose moat comes from workflow ownership rather than hardware, Duolingo’s defensibility comes from controlling the learning loop: curriculum sequencing, motivation architecture, CEFR alignment, and real-time proficiency modeling. AI strengthens this loop rather than threatening it.

Indeed, AI is accelerating Duolingo’s product velocity. Curriculum creation that once required years can now be done in weeks. Token costs continue falling, enabling more AI-powered features to trickle down from premium tiers into mass-market offerings, improving both retention and eventual monetization. AI unlocks entirely new experience types—speaking partners, video dialogues, adaptive scenarios—that were previously impossible. This is a classic compounding flywheel: better product → more DAUs → better data → better AI personalization → even better product.

Valuation

Against this backdrop, valuation looks increasingly disconnected from fundamentals. Duolingo now trades at roughly 6x forward revenue and 18x forward EV/EBITDA—a stark contrast to its historical multiple and to peers in subscription consumer software. For a net-cash business growing 20–25% with high retention, global reach, improving margins, and significant AI leverage, these multiples imply either a stagnation scenario or outright decline. Neither is consistent with user trends outside UCAN, ongoing engagement strength, or the accelerating product roadmap. Even a conservative PEG framework applied to Duolingo’s long-term EPS growth potential suggests material rerating upside.

Looking forward, Duolingo is also in the early stages of expanding its TAM beyond languages. Math, music, chess, and children’s learning represent adjacent verticals where Duolingo’s existing infrastructure—game design, learning science, personalization, and global brand—can extend with relatively low incremental investment. Each new vertical increases LTV, reduces revenue concentration, and makes the platform stickier across households.

Taken together, Duolingo is not a company experiencing secular decline. It is a category leader choosing long-term strategic positioning over quarterly optimization—precisely the type of behavior that temporarily depresses valuation while preserving or enhancing long-term value. With expectations reset, a maturing AI-enhanced product, global growth drivers outside the U.S., and substantial optionality in new learning categories, the risk/reward has shifted meaningfully in investors’ favor.

The market’s current narrative—“AI threat, slowing DAUs, lower guidance”—captures only the surface-level disturbances. The more accurate interpretation is that Duolingo is entering a new era: one defined by accelerated product innovation, a deeper moat built on proprietary learning data, and long-term monetization that is likely to be far more powerful than the company has shown so far. Misunderstood moments like this often produce the most attractive entry points. Duolingo is not a broken story. It is a long-duration compounder that has been temporarily mispriced because the market is extrapolating short-term noise rather than long-term fundamentals.