Willis Lease Finance Corporation (WLFC) - Flying High

Willis Lease Finance

Willis Lease Finance (WLFC) is the leading lessor of commercial aircraft engines and provider of global aviation service operations for over 40 years. It’s a family run business with a market cap of around $1B. It lacks sell‑side analyst coverage, and is valued at a 60% discount to its nearest comparable (FTAI). Despite a 300% share price increase in 2024, the current market price still fails to reflect WLFC’s intrinsic value. We believe the supply demand imbalance within aviation industry will hold up better than people thought despite potential recession concerns, and the recent decline gives us an attractive opportunity to purchase WLFC at 5x forward earnings multiples and close to 1x book value.

Business Description

WLFC is a pure‑play aircraft engine lessor specializing in commercial narrowbody aircraft engines, which comprise 90% of its portfolio and serve approximately 60% of the global commercial fleet. As of year‑end 2024, WLFC owned 354 engines and 16 aircraft, and managed an additional 277 assets for third parties. Through strategic acquisitions, regional joint ventures, and reinvestment, WLFC has built a unique, vertically integrated platform centered on engine leasing. This ecosystem includes:

Maintenance, Repair & Overhaul (MRO) Facilities

Asset Management & Parts Sales

Fleet Management Consulting

These capabilities enable WLFC to operate more efficiently, especially in times of supply chain disruption and market volatility. Not only having the available engine but also having the capacity to repair old ones and offer on time engine delivery is what airline customers highly value and willing to pay a premium for.

The ConstantThrust program covers the cost and risk of jet engine maintenance by replacing a removed engine with a serviceable engine from portfolio. It saves airline customers significant time, money, and risk associated with engine-heavy maintenance. We expect more airlines to enroll in this program which offers Willis predictable future demand and capturing value throughout the lifecycle of an engine.

Supply–Demand Imbalance

IATA quantified the scale of the challenges facing airlines because of supply chain issues in its latest airline industry outlook:

Average age of the global fleet has risen to a record 14.8 years, a significant increase from the 13.6 years average for the period 1990-2024.

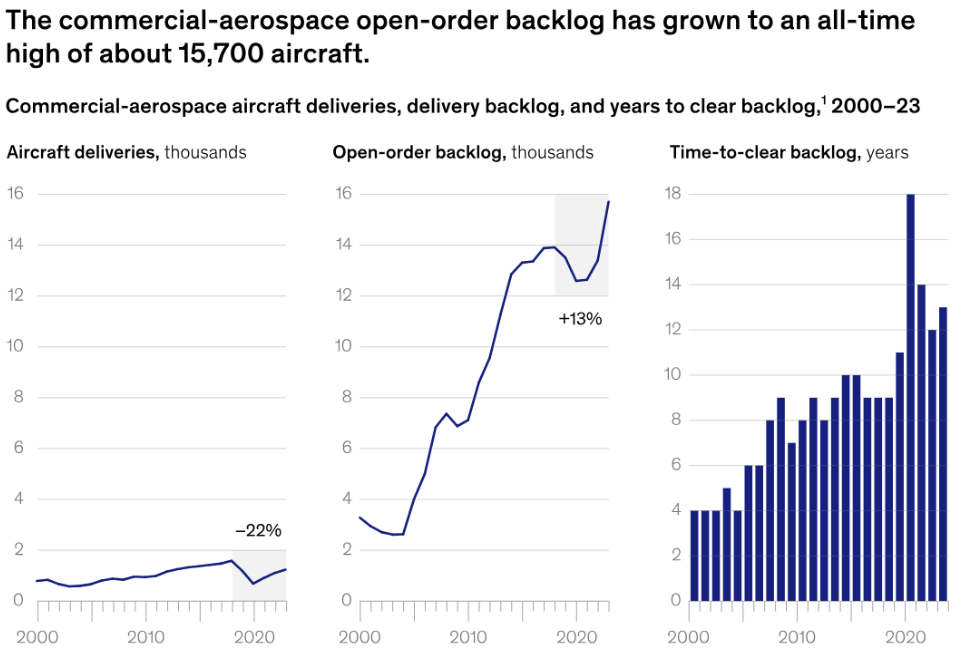

Aircraft deliveries have fallen sharply from the peak of 1,813 aircraft in 2018. The estimate for 2024 deliveries is 1,254 aircraft, a 30% shortfall on what was predicted going into the year. In 2025, deliveries are forecast to rise to 1,802, well below earlier expectation for 2,293 deliveries with further downward revisions in 2025 widely seen as quite possible.

The backlog (cumulative number of unfulfilled orders) for new aircraft has reached 17,000 planes, a record high. At present delivery rates, this would take 14 years to fulfil, double the six-year average backlog for the 2013-2019 period. However, the waiting time is expected to shorten as delivery rates increase.

COVID‑19 Impact: When global travel demand collapsed, the aircraft and engine supply chain shut down. Some facilities never reopened, and others faced chronic underinvestment. As air travel rebounded beyond pre‑pandemic levels, these capacity gaps created a severe supply–demand imbalance.

OEM Constraints & Industry Culture: Boeing’s quality‑control and cultural issues compounded supply problems. Aircraft production capacity is limited by the weakest supplier, affecting both Boeing and Airbus, and delaying order backlog normalization until at least the end of the decade. The recent tariff only further complicates the matter and I expect Boeing to miss its delivery guidance, causing further delays.

“The global aircraft shortage hampering airline growth will persist for four to five years as supply snags hobble production at jetmakers Boeing and Airbus,” said Air India CEO Campbell Wilson (Reuters, March 2025).

Boeing’s Darren Hulst counters that key supply‑chain elements will be in place by 2025 to stabilize output.

Ryanair’s Michael O’Leary noted, “In 30 years, I’ve never seen constraints to this extent—gearing up for 50 aircraft and only getting 30 was a costly lesson.”

MRO Delays & Rising Costs: Airlines now face engine shop turnaround times up 35% for legacy engines and over 150% for new‑generation models versus pre‑pandemic levels. These delays reduce fleet availability and drive up maintenance‑reserve revenues. Newer generation models are having more maintenance issues than initially expected due to design flaws, so they have to be send back to the shop to be reworked or be grounded.

Aircraft MRO have a large barrier to entry due tot the complexities of an aircraft engine and the high level of precision required to repair these engines, otherwise causing major accidents. The MRO shops have to be qualified by the OEMs and the qualification process can take decades to approve.

There is also a labor shortage because the repair staff are highly specialized and cannot be trained within a year. The existing talent pool is also retiring en masse so the capacity was further constrained.

“Aircraft engine MRO demand is likely to peak in 2026 and remain constrained through the decade,” warns Bain & Company, noting a surge in new‑generation engine demand around 2030.

Summary: With new aircraft scarce, airlines extend fleet lifespans, boosting engine‑lessor utilization despite higher lease rates. Constrained MRO capacity increases engine downtime, elevating demand for greentime engines and pushing market values—and corresponding lease rates—above pre‑COVID levels.

46% of Willis portfolio is short term leases (less than a year) so they can effectively reprice their leases to market when renewing the leases. This is much faster than the 5+ years for full aircraft leases.

The value for narrow body jet engine has increased significantly post covid recovery due to the strong demand and lack of new OEM supply mentioned above. Higher asset value means higher portfolio value for Willis ad higher lease rates. It currently stands around 2019 levels, and have further upside if supply demand balance worsens.

Why Engines Outperform

Engine is accounting for a higher percentage of aircraft value. The newer generation aircraft engines accounts for more than 40% of total aircraft value. And contrary to most people expected, it actually appreciates in value when it’s in production by OEM, which can span decades. When the aircraft approaches mid to late life, the engines have a combined value higher than the entire aircraft because engines are valued based on “greentime” and airframe on life span using straight line depreciation. Thereby making engine trading a profitable arbitrage opportunity if the company has the capacity to take down engines and rent them out to third party.

Razor‑and‑Blade Economics: OEMs price initial engines competitively but mark up LLPs and spare parts, driving midlife and terminal‑stage engine appreciation.

Resilience & Liquidity: Engines retain value throughout cycles and remain liquid assets. An engine trades for high single digits to 10+M dollars.

Technical Barrier to Entry: Engine leasing demands specialized expertise; mismanagement of LLPs or documentation can quickly erode asset value, limiting competition. Financial sponsors like Apollo and Mitsui provide the capital for engine lessors like Willis to deploy and manage those assets. There is a limited number of competitors out there.

“Engines are far more technically challenging than aircraft,” says ELFC CEO Richard Hough. “Without proper paperwork and condition control, you risk rapid value loss.”

Investment Thesis

Downside Protection: Market cap approximates liquidation value (book + engine portfolio + MRO facilities).

Lease Rollover Upside: Full lease rollovers into higher rates by end‑2025, with increased short‑term maintenance‑reserve revenues driven by tight MRO capacity and next‑gen engine demand.

Volatility Tailwinds: Long‑term maintenance reserves and gains on sale offer upside during market dislocations.

Next‑Gen Engine Leadership: WLFC is best positioned to capitalize on CFM56 retirements (~2026) and growing LEAP/GTF demand.

MRO Expansion & Program Penetration: Scaling ConstantThrust® and ConstantAccess® programs will boost utilization and maintenance‑reserve income.

Enhanced Investor Relations: Recent management initiatives to improve communications should attract broader coverage and narrow the valuation discount.

What we have underwrite in the model is:

One of the reason the stock dropped following most recent earnings is because the utilization did not match expectations, it declined compared to 2023 which raised a lot of question on the demand of this industry. We think it’s primarily because the large asset acquisition Willis did during the year, raising its asset portfolio value from 2.5 billion to 3 billion plus, growing by 20% above historical average. And notice its portfolio hasn’t grown very much since covid so they are returning to growth mode, they need to lease out the engines, which under current market conditions should be leased out relatively quickly at market rate.

Their portfolio utilization should return after 2025 1H to pre covid levels like 87%. This jump in utilization would give them significant operating leverage which increases the revenue and ebitda margins. It will also benefit their MRO repairs division. We assume lease rate remains around 1.3% and forecasts little incremental expansions since the introduction of Constant Thrust program was first of its kind and airlines are willing to pay premium for this turnkey service.

The stock price assumption is $120, we plan to buy at lower multiples, preferably close to 6x ($90+)

Valuation Considerations

WLFC depreciates engines on a straight‑line basis over 15 years to a 55% residual value. However, current market dynamics—asset scarcity, OEM pricing power, and maintenance demand—suggest engines should appreciate rather than depreciate. This creates a material gap between book value and intrinsic market value. Management estimates intrinsic value exceeds book value by approximately $600 million.

Given WLFC’s integrated MRO operations, active engine acquisitions, and dynamic lease‑rate adjustments, the company should trade at a premium to book value. Metrics like ROE (≈20% in Q3 2024) and FCF conversion (≈99%) better capture WLFC’s value than static book multiples.

Covid is a significant disruptor, even during the 2008 financial crisis the traffic only slightly declined. The overall trend is still up. Growing global middle class in India and China are still driving the flight traffic demand.

This time is different from before. Now, the backlog is entering a recession from an all‑time high, and it’s hard to gauge the impact. In the short term, supply certainly can’t keep up. Demand may weaken somewhat, but it won’t plunge. Look at 2008—it didn’t fall much because this is global demand, not just U.S. demand. Airlines rely even more on older aircraft, so there will be extra maintenance needs. Maintenance capacity won’t improve quickly, so engine leasing shouldn’t be hit too hard.

The biggest risk would be if Boeing suddenly gets its act together and starts ramping up deliveries, but I think that’s unlikely. Right now, lease rates are at the upper end of their normal range—they’re elevated but not absurd, especially since financing rates have risen too. More companies are choosing to lease rather than buy, or to do sale‑leasebacks. So the logic of utilization reverting to its typical ~88% is clear, with little downside. Lease rates should hold steady, and maintenance demand remains strong. Poor market sentiment may push valuations down, but that just makes good names cheaper.

We see that in the past it traded at about 5–6× P/E. In 2019 it was around 10× before COVID hit. So we believe a normalized multiple should be above 10×. Last year’s EPS was $15.50, so buying around 6× that—about $100—seems appropriate.

Then the target is 10× $22 = $220, essentially a return to its prior highs.

Investor Concerns:

Complexity of WLFC’s business model

Limited investor communications

Low free‑float liquidity

The 500M Share Issuance, what structure will the offering be (what percentage preferred at what rate?) And the usage of the funds(owner selling what percent, where to deploy this amount of capital in this tight market, can it be capital efficient?) And the reasoning behind such a huge offering remains unclear. I don’t know if it will be sucussfully executed without explaining the use of the funds.