Flutter Entertainment (FLUT) - Harvesting Mode

Recent Update 11/8/2025

The rapid rise of prediction markets in sports betting is a wake-up call to investors. Prediction markets operates an entirely different business model than Flutter and other sportsbooks. There is no market maker or book runner for each game, which means low operating cost because they don’t have to invest in expensive algorithm teams and purchase data from sports leagues to have an edge. It’s all free market activity, and history told us free market is always superior in prediction results than controlled ones. Sportsbooks is a controlled environment where the best performing bettors were kicked out, so does anomalies like those with insider information, but these are all free to access the prediction market, giving it much better predicting capacity. Also the liquidity at the market is always superior because someone is always there to fill your order, especially on NFL or other highly anticipated events, it can reach hundreds of millions in volume traded, active every second without much fees or delays. Third the accessibility of prediction market is unrivalled. They are legal in every 50 states, without much regulation. So they can avoid paying those high regulation cost to convince each state to open for sportsbetting. They are finding backing of industry titans like ICE and other powerful figures, so they are no longer the shady platform that only exists in the crypto world, but something much more open and trusted. They have wider reach to audiences because people can bet on anything from taylor swift to weather to anything that can think of. So this is much more engaging than only sports or online casinos, I felt people find much more confidence and fun betting on things they felt have an edge on, instead of roulettes or blackjack that they knew the odds were against their favor.

Sportsbooks have yet to turn to a profit but investors have been very patient, for the story they are telling, the steady cashflows, the casino 2.0 story, and the duopoly market share have been very appealing. But with the prediction market suddenly the story looks broken. I have yet to find a way how sportsbooks can win this race, or counter the erosion of marketshare from prediction markets. And the growth trajectory, or I should say the TAM for those states that have yet to open or yet to be mature are much lower now, considering that people would have adopted prediction markets earlier than sportsbooks. This impairs the story and have people doubt their long term growth.

Also, consumers are feeling challenged once again, bad omen for all discretionary names. There is really no hiding in this because consumer defensive like kraft heinz is also getting punished. So just like the rate hikes and worries of a hard landing recession in 2022, same valuation decompression is happening here to sportsbooks.

We think the industry is challenged and would refrain from investing until further clarity is reached. If Polymarket seeks to IPO, we are incentived to participate because we are anticipating a hype post IPO, much like Circle or retail favorites like Palantir. It’s closely tied to stable coins and deregulation of crypto industry. I believe it’s also profitable.

New era in Gaming

It’s not the first time we have looked at gaming companies. We previously looked at Churchill Downs, the host of the Kentucky Derby and the operator of many racetracks and HHM casinos in Kentucky and Virginia. They have benefited from the wave of deregulation after COVID, when the local government relaxed casino regulations and approved racetracks to operate slots within a nearby radius—ostensibly to support the local equestrian industry, or, to put it plainly, to generate tax revenue.

Although we ultimately decided not to invest in Churchill Downs—because the growth was already priced in and Virginia was loosening its casino regulations further to allow full‑fledged casinos with table games, thereby breaking the racetrack‑slots monopoly—a major takeaway was the profitability of casinos and how precisely they can estimate the daily win rate per machine or per table. The odds are fixed in the house’s favor, and there is no way gamblers can win in the long term. Were gamblers to see those statistics, they would likely feel foolish, taken advantage of, and regret their addiction.

Putting ethics aside, I think casinos are a wonderful business. They are addictive just like tobacco, sugary drinks, and alcohol. We all know how well these companies have performed over time; their resilience to downturns and stable cash‑generating profile demand attention from investors. One major flaw is regulation that is either too aggressive—taxing addiction businesses almost to extinction—or too loose, allowing overcompetition and declining economics. We have seen this repeatedly in history: Trump’s bankruptcy in Atlantic City was caused by nearby states like Pennsylvania opening for gaming, and Caesars’s bankruptcy was caused by a surplus of rooms on the Strip and lack of demand, which led to lower hotel rates and underperforming cash flow.

If we look at the history of casinos and how they have evolved, the first period—Casino 1.0—consisted of local gaming parlors, street‑corner bookies, and underground gambling joints filled with shady characters trying to make a quick buck. It lacked regulation, it wasn’t mainstream, and it was controlled by mobs. Casino 2.0 is Las Vegas, and we must thank Bugsy Siegel (as portrayed in The Godfather) for envisioning a desert oasis with legalized gambling for the GIs returning home from WWII. We must also thank Howard Hughes for wresting control from the mobs and running these establishments as legitimate businesses that attracted mainstream investment and created the grand vision of casinos we know today. The value proposition of Casino 2.0 is that gaming need not be shady; it can be relaxing—taking the family on a trip to Vegas, enjoying the shows and food, and playing a little. Casinos operate like tourist attractions with strong gaming monetization, but they are geographically constrained and subject to boom‑and‑bust cycles.

Moe Greene as Siegal

In Casino 3.0, we are witnessing the convergence of casinos with the stock market—that is, the biggest casino in human history. I saw the promise of online gaming (iCasino and iSportsbet), which mitigates many regulatory risks and achieves a scale and reach unseen before—a perfect combination of technology, gambling, and sports. I have not encountered anything as addictive as this business, and I am certain its total addressable market will soon surpass that of land‑based casinos and become a national addiction.

Companies in Casino 3.0—mainly Flutter and DraftKings—are technology firms more comparable to trading houses like Citadel than to their land‑based peers. They use models to predict sports outcomes and price options in their favor, just as Citadel sells options at wide spreads to retail buyers. Moreover, Casino 3.0 companies collect user data and recommend trading opportunities accordingly. They know each customer’s favorite teams and players, what they like to bet on, which sports they are watching, when their paychecks arrive, and when to nudge them to gamble further by offering rebates or credits. This is gamified Wall Street extracting the maximum from Main Street, while people enjoy playing and remain mesmerized by legendary wins. That’s why the title is called Harvesting Mode.

With access to large volumes of betting data, the Flutter risk team developed a predictive model of customer profitability. Paddy Power reckons that by the time a punter has placed 15 bets on horse-racing or turned over €500 in their account, the firm has a strong knowledge of how much it could expect to win off them. Aaron Rogan reveals that of 100,000 randomly selected Paddy Power customers as of 2018, around 40% would generate an 11-13% margin for the firm, with around two thirds of customers in the range 9-14%. Because bookmakers have the right not to take bets from punters who consistently win, the left side of the tail doesn’t stretch very far; not a single one of the 100,000 customers is expected to lose the firm more than 3%. Sure there are seasonal impacts when the popular team always wins, but that is sports and if we knew the best team always wins, it would not be interesting. Underdog to Hero stories are what get fans excited, and that’s what makes the books the most money. No team carries the league, there will always be shocker losses and wins, so a long term investor should not be concerned about short term seasonal volatility.

Casino 2.0 v. Casino 3.0

After initial heavy spending to acquire customers, legacy gaming operators realized that they don’t have the tools to price the sports bet as good as tech-native firms like Flutter. That means they are effectively subsidizing players by giving them better odds, which soon disrupts their economics. When the subsidization ends, players naturally switched to online platforms for better odds, more options, and better UI.

Flutter taking shar of MGM, pretty clear that Sports betting converts are the biggest source of new casino players and Flutter want to keep them within its ecosystem. The product itself are commoditized, with few tweaks of customization like customized slot games interface. Customer Royalty program is the key to keep engagements up, combing sports betting and casino is a clear winner.

Traditional land based casino operators just cannot compete. They are not technology focused and they lacked the scale to invest on par as Flutter or DraftKings, they have lost their early entry opportunity and their iCasino business are being cannibalized by Sportsbooks due to cross selling and generosity programs that aimed to convert Sports gamblers to casino gamblers, where they would have higher margin, and vice versa. I expect online native operators to keep eroding marketshare from traditional land based operators.

Field Research Takeaways

Won a 100x on slots off my 25 cent bet, lost 100 dollar on poker.

I conducted some field research by taking a taxi and asking several drivers—both white and Black—about their views on sports betting and online casinos. First, I asked, “Do you play these?” Both said they do, indicating usage is still rising. One said he had heard about it and wanted to play but did not know how—so that represents a potential future customer. My second question was, “Compared with traditional gambling, which do you prefer?” One driver said he prefers sports betting because he thinks it is more profitable; both said, “people make money there.” One driver even said, “Once I won 1,500 dollar.” I asked how, and he said he hit a multi‑leg parlay on underdogs—small‑probability events with very high returns. He felt it could make you rich. The driver who hadn’t played said he also thinks it could make you rich, since some people really do win. I believe there is an interesting misconception: winners brag, losers don’t, so the buzz leads people to believe it is highly profitable.

As for casinos, everyone knows the house always wins, so people accept that it is unprofitable for them. But “worth betting” (i.e., sports betting) is newer—people do not understand its mechanics well. They feel they have more control and a better chance than in a pure‑chance casino game. It is not just luck; they believe their knowledge of the teams gives them an edge. That is an illusion—just like stock trading: you tell yourself, “I know this company is great, others are fools,” and you bet big. In a casino, you know you have no edge, so you play casually, betting small. With sports bets, you feel more engaged: you watch the game, you root, you win or lose, and it keeps you happy longer. In a slot machine, one click and the money is gone—you feel nothing.

Another psychological trait I noticed is all transactions happen online, player deposits from their bank account, their balance shown in the app, and they withdrew to their bank account. Just like brokerage accounts, people rarely withdrew money unless they really needed it. There is this mentality that what’s in there stays in there and you want the balance to compound (not in a patient way but in a 10x10 parlay I will be a millionaire way). Casinos when you leave you have a cashout voucher and they give you cash, and you use cash to buy chips to play. Now you don’t even have a physical form anymore, it’s all digital numbers, people don’t really feel anything when they lose. And like all gambling stories, what they win from lucky strikes will always go straight back to the pot, costing them more in the process.

I just played slots and poker: I won on the slot and lost 100 dollar on poker. Both experiences were poor. The casino was old, smoky, and dark—no new equipment because regional casinos cannot afford big investments when returns are low. I hated being there. The betting speed was insane: the minimum bet was 25 cent; I was clicking about every ten seconds, losing over two dollar a minute. In an hour that is more than 60 dollar—so I would lose 30–40 dollar per hour. High rollers bet thousands at once, so their losses happen even faster. Five dollar lasted me under three minutes. It was a terrible experience. Sports betting feels more like the stock market: you place a bet and wait two or three hours for the result. You might even follow multiple games over days. That engagement—watching goals, wins, and losses—is compelling. From a customer‑value perspective, “worth betting” wins on convenience, experience, and the psychology of feeling in control. Its potential far exceeds offline casinos, especially over the next three to ten years, because everyone follows sports. Young people today are already gambling on options, sports, or both. It is highly addictive, and its market share will surely surpass brick‑and‑mortar casinos. The future is online “worth betting.”

A major takeaway is the “Value proposition” of sports betting to customers are much stronger than casino. A football game lasts for three hours or more, if you make it parlay, it could extend for days on different games. It ups and downs bringing your emotions with it, you can see the live odds and choose to cash out or hold. Every second you are betting, you are making a decision. This is just like options trading where there are huge swings intraday. This is a much better value proposition to me than sitting at a smokey shaggy casino waiting for my next pair of Ace to come, or endlessly scrolling the slots hoping I hit the next 100x. Online is the future, land based is the past.

CAC & LTV

The overall trend I observed and management told us is lower CAC, higher LTV. This bodes well for the business. The other day I was talking with my friend about valuation. He wondered why the valuation is so high when there is no profit yet. I said it is like Meituan issuing coupons: you spend money upfront on promotions, but over the customer lifetime it is profitable. In fact, many ads run by Flutter or DraftKings feature bet $5 and win $200 as an initial credit. This is to get people to be familiar with sports gambling, learn the features try their lucks, and later they will be hooked.

As sports betting spreads across more U.S. states, they need less marketing spend—everyone already knows about it—so incremental advertising costs fall. They are deploying national programs more than local ones because they have reached enough scale to run this efficiently. Note that National programs have a much lower cost per impression. They also use referral programs, the cheapest way to convert new customers. If you look at lifetime value in mature markets (legal for two to three years), margins keep rising, so new states will reach similar levels in a year or two. Spend‑per‑user grows about 20 % annually, showing players are betting more while the house edge falls—commercially advantageous, since higher spend means higher yield.

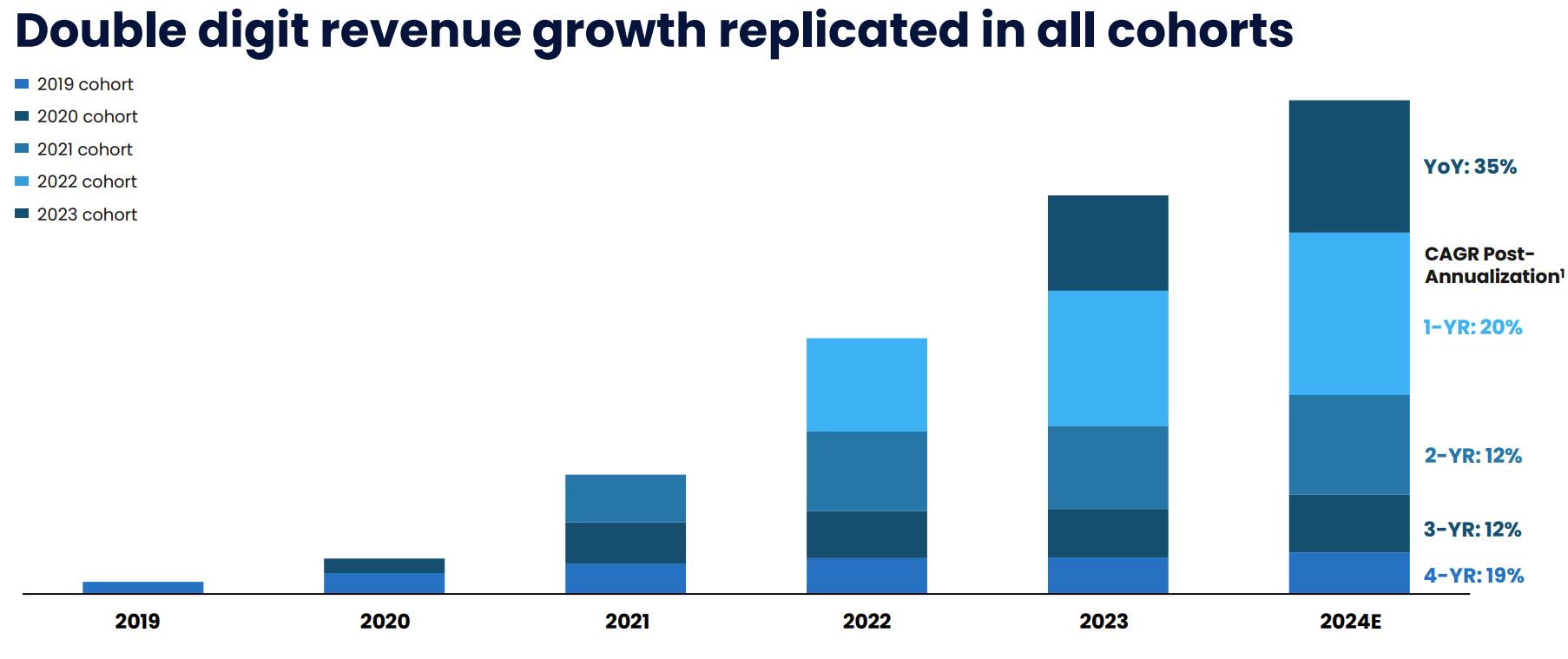

Very strong cohort growth rate, driven by increased Player Days, More money spend on APP, and Strong retention rate.

This shows how sticky sports betting are and how people naturally bet more. People are not going to not watch sports. When they watch, they want to gamble. Can’t avoid the thought of “ I wish I have bet on that I knew they would win” to “I wish I bet more on my parlay so the wins are multiples of what it is” and falling into the rabbit hole of " if I hit two parlays I could make a million dollars by 100x my money, easy generational wealth, even if I lose it’s no big deal.” Trust me, I have went through the option gambler’s mindset so I knew what it’s like.

Quantifying the Assumptions - Higher Penetration, Bigger Bets, Frequency, Hold Rate

After our previous discussions on why sports betting is such an addictive business that is superior to other forms of gambling and how it is poised for expotential growth over the years. It’s finally time we put it into numbers:

When we are talking about TAM, we are talking about penetration rate (legalization of new states, and existing state increased penetration), Average bet size (which correlates with consumer discretionary income and overall addiction level), Frequency (also related to addiction level), And hold rate (this relates to the algorithm of the bookie, parlay penetration, and multiples on parlays, general rule of thumb is the higher the multiple, lower probability of it hitting and higher the hold rate).

We are still early to realize how big the TAM is for United States. Flutter recently upgraded their TAM from $40B to $70B by 2030. That is largely the result of increased casino penetration and player value realization. After TCL, I have learned my lesson to not trust management assumptions and do my own channel checks. I read analyst research reports, state gaming reports, and gaming related forums to collect data that formed my own estimates on TAM.

Americans are crazy for sports, from talking to consumers and sports investors I know this is a growing industry. When we look at the age distribution of sports bettor, over half are under the age of 34, highlighting how young this industry is. Long term, I think it’s fair to assume higher sports betting participation and higher spend per player (frequency x average size). People are addicted to so many things right now, they have a shorter attention span, impulsive behavior, and reduced logical reasoning capacities. Sports is the way of grabbing their attention, and their wallets.

To Help people visualize the inherent assumptions $50B operator revenue TAM would imply:

1. Arguing higher penetration to 25% from 20% as sports betting become more relevant & Sports Betting Deregulation as treaties with Tribes were struck and remaining states deregulate, doubling the applicable population (with online casino being the extra option as they are more profitable)

A broad Siena College poll finds 22 % of U.S. adults hold an active online sports‑betting account and the American Gaming Association (AGA) reports 21 % bet on sports in the past year . With roughly 246 million adults, 19–22 % penetration yields 47–54 million active sports bettors.

Statista estimates 7 % of U.S. adults played online casino games in 2024 . That implies 17–18 million active online‑casino players. Combined, the overall online‑gambling user base is on the order of 65–72 million unique individuals today.

We held the approval of Texas or California for sports betting as a growth option. I believe the market is so big and so lucrative that it’s impossible for the tribes, which hold significant influence in local gaming board, to ignore. They don’t have the capacity to offer the same level of service as Fanduel or DraftKings, so I believe they will work out a revenue sharing model where the take a cut from the profit pool.

2. Arguing Handle per user will increase similar to mature state level (4-5k) while mature states will further increase (Note: Hold % = sportsbook revenue / handle). Also seeing meaningful long tail user increasing spend

We are seeing healthy double digits handle growth across the board from Iowa to New York.

We note the average handle is 4k to 5k. Given healthy growth I think it’s reasonable to assume average of 4k handle.

3. Visualizing the 5k handle per player: uneven skew towards the top spending cohort

Note the data was published in 2021, now the handle have massively increased, it was shown to showcase the skew towards top 10% spenders that contributes 80% spend

Just like any other addiction business, Sports gambling preys on the weak, those who have an addiction.

"The top 10 percent of American drinkers — 24 million adults over age 18 — consume, on average, 74 alcoholic drinks per week," Washington Post reported. "That works out to a little more than four-and-a-half 750 ml bottles of Jack Daniels, 18 bottles of wine, or three 24-can cases of beer. In one week." This averages out to roughly 10 drinks a day. This cohort contributes 60% of sales.

So if we assume the 90 percentile contributes 80% of all spends, similar to alcohol levels, that leaves the remaining 90% with 20% spend level. At 50 weeks per year, even a single $50 weekly bet yields $2,500 in annual handle. I think the remaining 80% have long runway to increase their spend and frequency. The mass advertising campaign are fueling this trend. If the remaining 80% can lift their spend, the long tail would meaningfully lift the overall handle revenue.

Sports‑betting frequency: 59 % of sports bettors wager at least weekly, and 24 % bet three or more times per week The median bet is $50.

Casino frequency: 48 % of online‑casino players gamble multiple times per month and 58 % at least weekly . so $40–$50 of bi-weekly play easily sums to $4,000–$5,000 per year.

4. Conclusion (Fanduel Hold rate is 16% minus 4% generosity rate, future projected to increase hold rate)

By 2030, as more states legalize both sports betting and online casino, penetration can reasonably rise into the mid‑20 % range for sports and low‑teens for casino, bringing 70–80 million users. At $4,000–$5,000 annual wagers per user, that yields a $280–$400 billion gross handle market—of which 10–15 % hold . If we do a 50/50 split with iCasino, that represents an estimated TAM of $60-70B.

We are already seeing this level in mature states like NJ, PENN, Mass. Where 20% penetration rate + $5,000 annual handle, it’s a matter of time for newer states to mature to similar levels.

Median is around $50, if we forecast higher addiction, there should be more skewed to large ticket sizes.

Fanduel has structurally higher Hold rate compared to DraftKings. And Casino 2.0 Player are just lagging behind the pack, validating my thesis that they were incapable of adopting to Casino 3.0

Valuation - Endgame 2030

I was little confused at first because I saw this wide discrepancy in valuations for Fanduel. Some are still using the revenue multiples approach because Fanduel historically did not reach profitability and it still is rapidly growing, so people thought it’s a good idea to value it like a tech business. And the other camp is the fundamentalist approach, they are saying revenue multiples are too high and aggressive and Fanduel should be valued on Ebitda.

If we assume no market share expansion, which I thought was pretty conservative especially on the icasino front as cross sale and royalty promotions attract more customers. Fanduel will control 35% of the $50B GGR TAM, which equal to 18B.. adj. margin of 25%= 4.5B, If we assign a conservative valuation 15x, the US business is worth 65B. If we do 10x for conservative purposes, Fanduel is worth 45B.

Non-US Value of $25.4B Using 2026 EBITDA Multiple. We value its non-US operations at $25.4B by applying a 9.5x EBITDA multiple (lower vs. our previous 10x) on our 2026 EBITDA estimate for its non-US EBITDA of $2.7B. We use 2026 (vs. 2025) largely to incorporate FLUT's pending acquisitions in Brazil (NYX) and Italy (Snai), which we have incorporated into our valuation. I think by 2030, assume 8% annual growth rate, it should be worth 35B.

35B+45B=80B for conservative case, and 65B+35B=100B if we buy at 43B*0.75=32B, our IRR is 20% for conservative and 25% for upside, matching out return hurdle rate.

Pricing

The support appears to be $200 for several reasons, first the up trend line finds support at this level, also if you look at past cycles, forming an inverted head and shoulders pattern, the neck line is around this level, third if you look at recent drawndown due to tariff, investors seem to find support at this level, and this is a whole number so psychologically it’s hard to break.

But in the case of stagflation and broader US inflation, I expect the market to panic and break those support and find support at 180 line, I think a 30% drawndown from the peak for a gaming company that is heavily exposed to consumer discretionary income is not enough, it has more room to run into the 40%, indicating 180.

Note that the previous 2022 rate hike cycle we saw a 50% drawn down from the peak, so this stock is volatile. I would prefer to build initial position at 200 level and increase to full around 180. Given the 9 EPS for this year and 12+ next year, I think 20x or 22x multiple are pretty reasonable.

The online sports betting industry have surprisingly be resilient during economic downturns. If we disregard Covid and go to financial crisis period, they did not really fell that much, which is kind of puzzling because people would assume less discretionary income means prioritizing remaining income to food or housing. But I guess gamblers, especially those who are addicted, can’t really stop and they would rather skip meals than skip gambling. But regardless, market punishes this sector due to unfavorable macro trends and I think Flutter can’t avoid the selloff.

In terms of allocation, if Draftkings fell to attractive levels, I think we could allocate 30% to Draftkings to caputre the rebound. But the majority should stay on Flutter because I like the international exposure which hedges country macro risk and loss or taxation changes in specific country. It’s cashflow is much stronger and it’s hold rate remained industry leading, and we are seeing great trends of Flutter capturing shares in the iGaming market, the more profitable one. I like the brand, the global platform, the price to multiples, the execution and their technology leadership.

I asked Chat and here are its response:

Consumption of sports betting holds up in downturns largely because core bettors treat wagering as a habitual “leisure staple” rather than a luxury, and because digital platforms make it easy—and sometimes psychologically compelling—to continue playing even when budgets tighten. In economic‑terms, sports betting exhibits low (or even negative) income elasticity: demand falls much less than overall income, and in some cases rises among those seeking quick gains. Key drivers include:

Low Income Elasticity of Demand

Nevada data estimate a long‑run income elasticity for sports betting near 0.5, meaning a 10 % drop in income cuts wagering handle only ~5 %.

Similar studies in retail gambling find that lottery and pari‑mutuel bets often have near‑zero (or even negative) income elasticity—players may gamble more when feeling financial stress, seeking a windfall gain.

Shift to Luck‑Based, Low‑Cost Bets

During recessions, gamblers migrate toward low‑stakes, high‑jackpot games (lotteries, scratch cards), which require small outlays but offer large potential returns. Sports bettors likewise gravitate to small‑wager parlays or micro‑bets that feel “affordable” yet exciting.

Digital Convenience & Engagement Tools

Mobile apps reduce friction: with a few taps bettors can place wagers, reinvest winnings, and chase losses—sustaining activity even when discretionary budgets shrink .

Features like “auto‑bet,” “cash‑out,” and personalized promotions lock in engagement and create habitual patterns resistant to income shocks .

Promotions and Loyalty Programs

Operators maintain or even increase free bets and rebates during downturns to retain top‑value customers; these incentives cushion the impact of lower disposable income on wagering frequency .

Psychological Factors

Financial stress can drive “gambling as coping”—people gamble more when anxious about money, hoping for a quick solution, despite long‑odds .

Cognitive biases (illusion of control, gambler’s fallacy) intensify during downturns, as bettors overestimate their edge and chase losses .

Empirical Evidence from UK & Australia

In the UK 2008–09 recession, off‑course sports‑betting GGY rose 2–3 % despite GDP declines, while land‑casino revenues fell briefly before rebounding .

Australian total gambling turnover grew 18 % in 2022–23 amid high inflation, and sports‑betting turnover hit record levels—even after venue closures—driven by online channels .

Regulation Risk

Regulation have an outsized impact on profitability than macro. Sports betting is newer, but the pattern is similar: very high rates can backfire. Early adopters chose 6–20% of net revenue, which operators say keeps the black market (illegal bookies) in check. A few states (NH, NY, RI) pushed rates to 51% for online betting, prompting warnings that bettors will avoid legal apps. Indeed, when states have pushed cigarette taxes too far, illicit markets exploded, suggesting a practical ceiling for taxation.

I think it remains the biggest risk and I would like to see more proactive actions on lobbying to protect shareholders from this risk.

The Betting and Gaming Council argues rates above ~20% hollow out the regulated market; MPs reliant on tax revenue and racing interests may push back. Previous extreme top‑rate experiments (e.g. 70% casino duty in 2007) were later rolled back, suggesting a de facto ceiling near 25%–30% before adverse effects force a reversal.

I think sports book operators can handle a tax rate that is below 20%, that' is embedded in the business model, but if it’s higher than that they would have to put surcharges on customers, leading to lower spending.

Missouri (2024): FanDuel and DraftKings collectively contributed over $40.5 million to support the "Winning for Missouri Education" They were capable of offering big budgets to get their goals passed. I expect the political influence of gaming operators to get bigger, surpassing that of the opposing land based casinos in future as their size have shifted.

Prediction Markets Risk

Brent Montour, Analyst, Barclays: Good afternoon or good evening everybody and thanks for taking my questions. So the first question is on the prediction markets. Hoping Peter you could just address all the chatter out there and with the roundtable canceled what is the next sort of milestone or event that we should all sort of be keen in on the next I don’t know weeks and months? And the second question is another question you were asked earlier just to ask it a different way. This is the first quarter was the second quarter of very better favorable results.

So there’s a lot of betters out there with a lot of cash in their accounts. Is it wrong to look at that as sort of de facto added resiliency in the balance of your guidance and your operational sort of outlook knowing that those folks have flush accounts?

Peter Jackson, CEO, Flutter Entertainment: Afternoon, Brent. Let me start with the prediction markets question. It’s I’ve said this to people before, but it’s worth reminding you, we do operate the world’s largest sports betting exchange. So we know this space well. The Betfair exchange has, for many years, given us very good insights in terms of how this stuff can play out.

And look, I think it tells us that you’ve got to be quite thoughtful about how exciting the exchange product can be when you have a fully fledged sports betting product available to you. We can see how important the parlay mix is to a U. S. Audience. And of course, you can’t access that in the same way with something like the exchange.

So we’re very thoughtful about it, particularly having seen so much success in terms of having the best product in the market. And I think that for existing states where sports betting is allowed, I’m not that confident that this is a sort of will have a sort of significant impact. But I think there are new markets which could become available to customers in say, so as Volkswagen’s already allowed. The political stuff is something that people talk about and other gamified markets as well. So look, we’re interested in the potential opportunity.

We have brought some of our team who have experience in building these products and services from the Betfair exchange business and put them into Fanduel to help us evaluate the opportunity. Look, we’re working through it. Clearly, in states that haven’t regulated, there’s a sort of prime the pump type of opportunity that is not that dissimilar to some of the DFS stuff, albeit it’s worth remembering that DFS is a really good precursor to the parlay product, whereas the prediction markets are quite limited. So look, it’s we’re interested in potential opportunity. There’s puts and takes, we’re working our way through it.