Streammax (SZ002970) V. Samsara (IOT) - A study

This article is also published on my Snowball account in Chinese

https://www.horizonscapitals.com/s/David-Streamax.pdf

Pioneers in Commercial Vehicle Intelligence

The market has deeply explored intelligent solutions for passenger vehicles, identifying numerous software and hardware companies related to smart cockpits and autonomous driving—such as Desay SV and Hesai (Lidar). However, commercial vehicle intelligence remains relatively underexplored. As an investor in BYD and a believer in Chairman Wang’s vision, I’m confident that the wave of electrification and intelligence will also sweep into the commercial vehicle sector. Technological innovation is meant to be shared and inclusive—it’s inevitable that it will reach more B2B sectors.

This led me to Ruiming Technology (SZ002970) or Streamax, which I consider China’s leading commercial vehicle intelligence company. It aligns perfectly with my long-term investment strategy focused on “high-tech, specialized, and globally-oriented small giants in manufacturing.” I’ve also studied Samsara (IOT), a U.S.-based company seen as the first public commercial vehicle intelligence firm. Despite differences in business models, their products share many similarities and are worth analyzing side by side.

Market Trend: Video-Based Fleet Telematics

Integrating cameras into commercial vehicle environments for video-based solutions is a major trend in fleet telematics. Berg Insight defines "video telematics" as a broad set of camera-based solutions for commercial fleets, implemented either as standalone systems or as add-ons to traditional telematics systems.

North America leads this market, with a size over three times that of Europe, which is mostly concentrated in the UK.

North America: In 2023, about 4.9 million video telematics systems were in use. By 2028, this is projected to grow to 11.7 million at a CAGR of 19.0%.

Europe: In 2023, about 1.4 million systems were in use, expected to reach 3.1 million by 2028 at a CAGR of 18.0%.

In North American trucking company earnings calls, management frequently mentions two key investment areas: expanding sites and fleets, and upgrading technology—covering logistics software, GPS, cameras, safety systems, and software subscriptions.

Fleet management system penetration is expected to grow from 53.3% in 2023 to 80.6% in 2028.

In Latin America, fleet management system usage is expected to grow from 6.5 million units in 2023 to 13 million in 2028, at a CAGR of 14.9%, with penetration increasing from 19.1% to 36.7%.

Samsara’s Market Insight

Samsara CEO Sanjit Biswas notes the immense opportunity: the U.S. has 30 million commercial vehicles, most of which are not connected to data systems. Samsara’s plug-and-play solutions offer high ROI and easy installation via diagnostic ports.

With rising penetration, this market is growing fast. Demand for hardware and software is surging, with a shift from aftermarket installation to factory integration (OEM pre-installation), accelerating intelligent adoption in commercial vehicles—not limited to trucks, but also taxis, construction vehicles, buses, and specialized vehicles like cranes.

China’s Challenges & Opportunities

China lacks advanced fleet digitalization. This is primarily due to cost factors. In the West, high labor and equipment costs—and expensive liability risks—make ROI on fleet upgrades obvious. In contrast, China’s lower labor costs, low incident costs, fragmented market, and thin margins make SMEs reluctant to invest in such systems. Even when they do, due to their fragile financial health, Streammax sometimes face difficulties collecting on the receivables. And in an interview Streammax CEO has criticized To-G projects for not being entirely merit based but based on connections with public officials. They don’t really care about the quality of the project and the cost savings, so it’s harder to win project mandates on quality alone.

However, Chinese policy is mandating safety systems like DMS and emergency braking (AEBS), which benefits companies like Streamax. This also explains why its main growth is overseas, while domestically it's more focused on government (To-G) projects—real profits come from B2B.

Side note: China's fragmented logistics industry also fostered platforms like YMM, which is the Uber for trucks, serving as a platform that integrates logistics capacity and shipping demand. It’s a wonderful business model and I’m invested in that too.

Business Model Comparison

Samsara: SaaS subscription-based. It doesn’t profit from hardware (outsourced to Taiwanese manufacturers), focusing on software design and optimization, plus local sales and support. Recently turned profitable. Its high valuation (12x PS) reflects the market's preference for SaaS businesses.

Product Comparison:

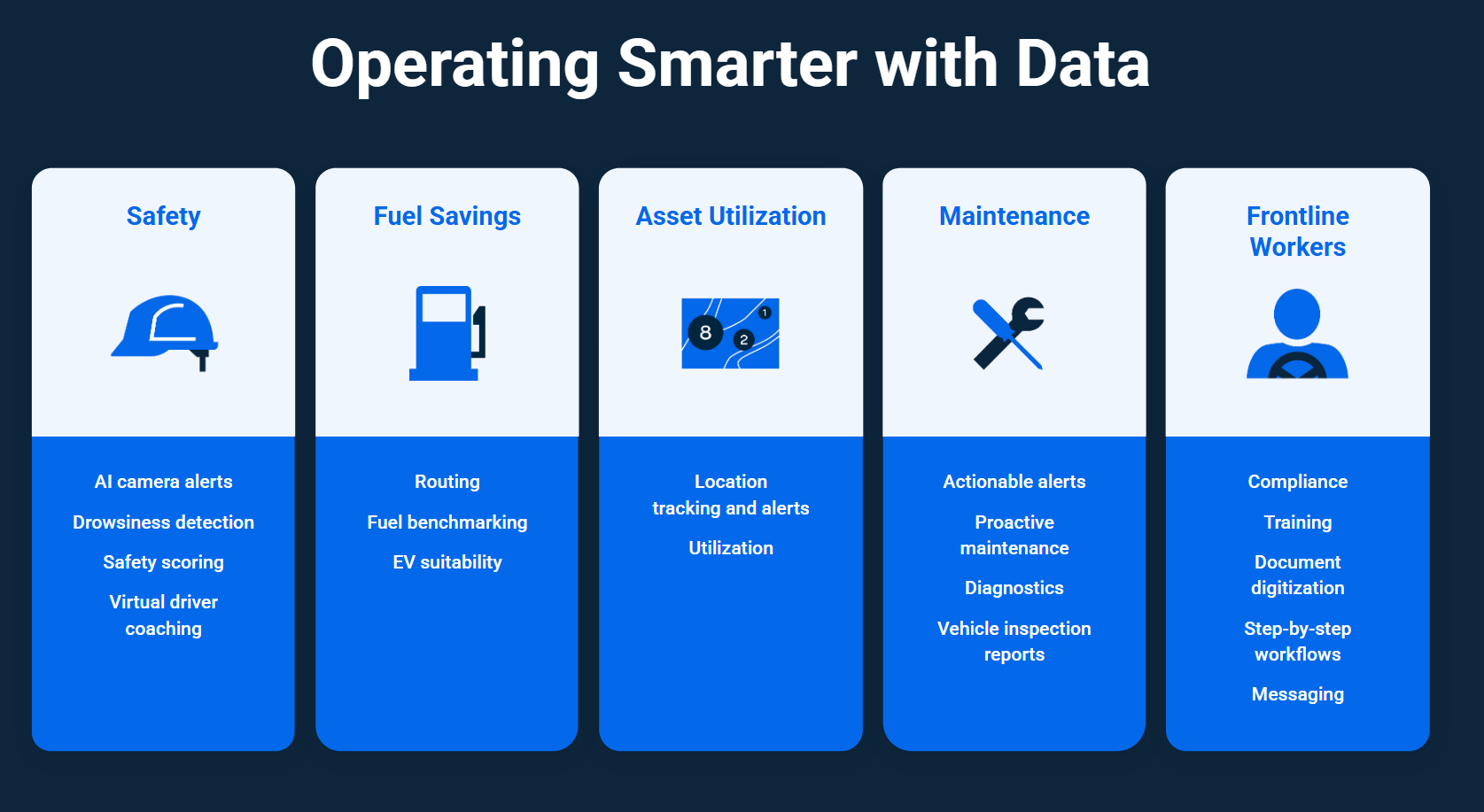

Despite differences in model, Samsara’s product line is very similar to Streamax’s—aside from Samsara’s frontline worker app, 70%+ of its revenue comes from safety management and telematics. For Streamax it’s a hundred percent because they recently divested their electronics processing unit which is lower margin and uncorrelated with its main business lines. However, we do see Streamax branching out to develop new functions like Compliance Apps and sight monitoring AI.

Streamax: Manufactures its own cameras, MDVRs, core processors, and has its own software platforms like Vision Zero and FT Cloud. Located in Shenzhen, next to BYD and other innovative firms, Streamax benefits from the regional ecosystem and talent pool. Its potential in commercial vehicle software rivals Samsara’s, especially with partners like Momenta, bringing high-level assisted driving features onboard.

While AEBS is hard to retrofit (due to powertrain integration), Streamax partners with OEMs like Yutong Bus to integrate it from the factory—this is a positive sign. Securing more OEM deals abroad would be even better. If domestic policy expands retrofit requirements, that’s another plus, though it’s currently encouraged, not mandatory.

Transition from Hardware to Software

Streamax has begun its transition to software, per investor Q&A highlights, this could lead to higher margins and valuations:

AEBS solutions are already sold at scale to public buses and taxis in China.

Certified by EU third-party agencies, ready for EU mass sales post-July 2024 when EU safety standards become mandatory.

Already has fixed-point cooperation with multiple Chinese and two foreign OEMs in EU.

Their EU-standard solution may eventually expand to passenger cars as well, leading to OEM installations and potential partnerships.

Sales Strategy & Business Comparisons

Streamax uses a “direct-managed, indirect-sell” approach:

Influences end users with product performance.

Partners with system integrators/operators for sales and maintenance.

In China:

Direct users include local bus/taxi companies (especially in Shenzhen).

Operates maintenance teams locally.

Most domestic sales are via integrators.

In overseas markets:

Products in over 100 countries.

Due to scale, relies heavily on integrator/operator partnerships (“one country, one policy” approach).

Nearly no direct overseas customers.

This model reduces operational costs and scales more efficiently. This explains why Streamax was ranked number one in MDVR sales yet it’s little known abroad, because it does not directly face the end user. Streamax’s domestic business has some direct sales, but integrator sales dominate due to servicing constraints.

Samsara directly services its end customers, taking a subscription model and have hands on deck to address any problem that comes up during the integration and application process. They do not manufacture their hardware. They are more focused on designs and software customization.

This reflects the difference between US and China business models. Chinese companies have manufacturing and they are developing software capacity, thereby moving up the value chain and capable of taking on the whole project if the on-the-ground team has a strong presence. US businesses focus on the software and design, the higher-margin parts. And their customers have much higher willingness to pay due to higher labor costs and regulations. They are valued differently in the capital market—one is viewed as a manufacturer with a 20x PE, $1.3B valuation; the other as a SaaS provider at 12x revenue, $26B valuation.

Of course, one can argue that Samsara is making USD and its business is more lucrative, but fundamentally, in terms of products and the software stack, I don’t think the two differ that much. I’m not saying Samsara is overvalued, but I am saying US companies have a much higher operating expense—sales teams, compliance, customer success, stock-based compensation, and branding. These all drive up cost structures and, consequently, the price tags they command.

In contrast, Chinese firms are still seen as cost-efficient solution providers rather than innovation leaders, even though their products may be functionally comparable. This valuation gap is not necessarily a reflection of product quality but rather of narrative, market positioning, and regional economics. The Chinese company is perceived as a manufacturer moving into tech, while the American one is seen as a tech company first—even if the deliverables are nearly the same.

EU Market Potential

From July 2024, new vehicles in 20+ EU countries must meet EU safety standards. Streamax has:

Signed deals with several Chinese OEMs for EU-compliant products.

Already receiving and shipping EU-compliant orders.

Collaborating with OEMs in Turkey and others across Europe.

Non-EU countries like Japan, Australia, and Mexico are also adopting EU standards.

Streamax is one of the few Chinese companies fully certified for EU standards, positioning it well for international growth. It’s much more reliant on international expansion, contributing close to 55% of revenue and I expect this share to grow as international market have stricter regulation compliance and higher labor/insurance costs. The investments in IoT have higher ROI, even if it’s not mandated by the government.

While Samasara still focuses on US market, which is underpenetrated and very lucrative. It’s international sales contributes less than 20% of total revenue.

Competitive Moat

Yes, others offer hardware-software integration, but few offer complete systems. Customers prefer a unified platform over pieced-together solutions. Most rivals lack R&D capabilities and real-world case studies—critical in high-barrier B2B/Gov sales.

Sold over 4 million MDVR units, leading market share.

Has hardware strength, extensive use cases, and real-world data to optimize its software.

Offers custom solutions tailored to specific vehicle types and regions.

Their Vietnam factory is modern and highly automated. The founder avoids media but showed strong responsibility and long-term thinking in a rare 17-minute interview. R&D spending is 16% of revenue, with a customer-first mindset—similar to Samsara.

He said, “After going public, the stock dropped and performance suffered. People said I cashed out and no longer cared. That pressure made me want to prove otherwise. I’m not someone who sells out. Our performance has since improved.” 2021–2022 results were hit by chip shortages and global COVID disruptions—temporary issues that don’t affect long-term growth.

MDVR as the Core

Streamax’s MDVR is the “brain” of commercial vehicle intelligence. It’s not just a recorder—it integrates:

DMS (Driver Monitoring): Detects fatigue, distraction, gives real-time alerts.

ADAS: Lane departure, forward collision warnings, etc.

BSD (Blind Spot Detection): Prevents side collisions.

Edge Computing: On-device data processing for faster response.

This makes it a smart terminal, not just a data collector.

Conclusion

If you follow our investment philosophy and the businesses we wrote on like Shemar electric, Richful Lubricant Additives, and Streamax, hopefully you will recognize a pattern.

I favor companies that pursue both overseas expansion and domestic substitution. They should be small, specialized players with dominant positions in their perspective markets, representing the rise of “Advanced Manufacturing in China. However, "going global" does not just mean exporting products—it means exporting production capacity, including capital, technology, and labor, and acquiring experience in dealing with foreign clients. Following the basic law of economics, only when you exchange with other countries can surpluses be realized, I view the surplus as extra profit margins. In the case of BYD, it’s selling cars to EU at nearly double the price, triple the profits, yet still undercutting comparable models in both price and performance. This is the power of consumer surplus, by focusing what you done best and facilitate international trade, preferably direct sales without middle man.

Growth drivers:

Domestic: Policy-driven retrofits of commercial fleets.

Overseas: Expanding market share, more direct full-suite orders, tailored product development.

The trend toward commercial vehicle intelligence is clear and accelerating.

EU-standard expansion:

OEM partnerships for pre-installed systems.

Entering European markets via Chinese vehicle exports.

Pilots in Turkey and other EU nations progressing.

Japan, Mexico adopting EU benchmarks too.

2024 front-end revenue: ¥96.95 million, up 119.8% YoY.

With increasing OEM adoption of intelligent systems (AEBS, domain controllers, e-mirrors), pre-installation is accelerating.

Software growth: If AEBS and ADAS (commercial vehicle-specific) sales rise, margin and valuation will improve.

Valuation

Given similar growth rates, I compare Streamax to Desay SV (hardware + software for passenger cars), which trades at 20–25x PE. If exports take off, it could reach 30x PE.

With 2025E EPS of ¥2.5, target price is:

Conservative: ¥60

Bullish: ¥75

Why I prefer Streamax over Desay SV:

Less competition in commercial space

Higher barriers to entry

Stronger overseas exposure

Not tied to a single OEM’s volume

Software potential not yet fully realized

A friend of mine asked if autonomous will make them obsolete, I thought it’s a really good question, and probably puzzles a lot of investors, so I thought I would give it my take.

Response to: Will Autonomous Driving Make Streamax and Samsara Obsolete?

1. Autonomous Driving Is Still Distant for Commercial Vehicles

While autonomous technology is advancing, full autonomy—especially in the diverse and complex commercial vehicle sector—is still many years away. Passenger cars on well-mapped urban roads are a very different challenge from commercial trucks, buses, and specialty vehicles operating in unpredictable, high-variability environments. Regulations, liability, infrastructure, and safety concerns will slow adoption significantly.

2. Commercial Vehicles Are the Last to Transition

The commercial vehicle segment is incredibly diverse: from long-haul trucks to construction vehicles to municipal buses. Each has unique operating environments and payload requirements, making a universal autonomous solution extremely difficult and expensive. Integration complexity, fleet turnover timelines (often 10–20 years), and union resistance (due to job loss fears) all point to a gradual, not disruptive, adoption curve.

3. Streamax and Samsara Will Likely Evolve, Not Be Replaced

Rather than being made obsolete, companies like Streamax and Samsara are positioned to evolve alongside autonomous technology:

Streamax: Provides hardware and edge AI systems (cameras, ADAS, DMS) that remain crucial for both human-driven and semi-autonomous vehicles. These systems are integral for regulatory compliance, insurance, and fleet monitoring—functions that do not go away with autonomy.

Samsara: Offers data integration, analytics, and fleet management software. In an autonomous world, real-time operational data becomes even more valuable. Samsara can pivot to serve autonomous fleet coordination, diagnostics, and regulatory reporting.

You correctly point out that the future ecosystem will be collaborative, not vertically integrated by a single automaker. A realistic future setup might look like:

Streamax supplies ruggedized camera and sensing hardware.

Moment[a] or similar companies provide autonomous driving software layers.

Samsara integrates everything into a usable platform for fleet operators.

4. Historical Analogy: EVs Didn’t Kill Oil Overnight

Your analogy with oil vs. electric vehicles is excellent. The transition is gradual, and legacy assets (in this case, existing commercial fleets) don't disappear just because a new technology emerges. Autonomous vehicles will coexist with traditional ones for decades.

5. Regulatory Drivers Still Favor Current Solutions

Global safety regulations (like the EU’s GSR requirements) are pushing for immediate upgrades—cameras, ADAS, driver monitoring, etc.—regardless of future autonomy. Streamax and Samsara are well-positioned to capture this demand now.

6. Avoiding Paralysis by Futurism

You're wise to caution against being paralyzed by long-term forecasts. Investors and operators should focus on what generates value today and over the next 5–10 years. Right now, making commercial fleets safer, more efficient, and compliant is a major value driver.

Appendix: I’ve also included some charts and excerpts from the annual reports of both companies for comparison.